Revealed: Public sector most exposed to risk from rising energy bills

- Details

The Culture, Leisure & Community sector is the most energy‑vulnerable property sector in England and Wales. Search Acumen explores the results of the analysis.

- Nearly a third of buildings in the Culture, Leisure & Community sector fall below the legal minimum energy standard, data shows, leaving the public sector exposed to high risk from rising energy bills

- Half of Local Authorities have registered a non-domestic EPC with an F or G asset band in the past five years

- Fewer A, A+, and B EPCs were registered in 2025 than in the two previous years, down 22% from a 2023 record high – showing the pace of compliance is slowing

- In the first two months of 2026, 200 commercial buildings have registered with an ‘illegal’ EPC, failing to meet MEES regulations

- Search Acumen: “Cooling financial climate and rising energy costs are slowing the race to retrofit”

The Culture, Leisure & Community sector is the most energy‑vulnerable property sector in England and Wales, new analysis reveals, leaving Local Authorities at risk.

Nearly a third (28.5%) of non-domestic buildings within the Culture, Leisure & Community sector lodged one of the lowest EPC grades of either an F or G in the past five years, falling below the minimum standard of E - by far the largest proportion of all commercial property sectors [Table 1].

As oil and wholesale gas prices spike worldwide, operational costs are rising fastest for the most inefficient buildings. For Local Authorities that look after key community assets in this sector, including museums, libraries, theatres, and public leisure facilities, the added financial pressure paints a concerning picture for councils already struggling to pay the bills.

Gas intensity within the Culture, Leisure & Community sector is 115 kWh/m², the equivalent of fully charging your phone over 10,000 times for each square metre, every year, meaning these buildings are still heating‑dominant, making them especially vulnerable to high oil and gas prices, even if electricity intensity is low[1].

The analysis, conducted by property data provider Search Acumen, also examined the largest sector contributors by volume to EPC ratings below an E. The office sector ranked the highest, with more than 3,500 buildings falling into bands F and G over the past 5 years [Table 1].

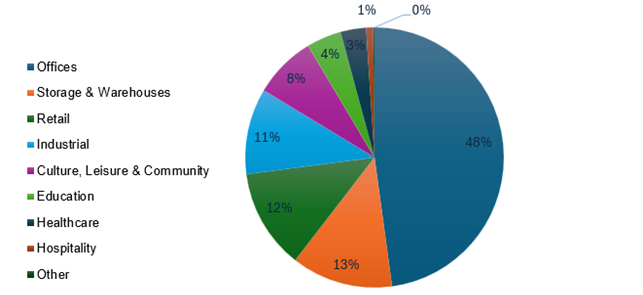

Furthermore, in 2025 alone, the office sector accounted for almost half (48%) of all F and G bands lodged, risking voided tenancies and obsolescence [Chart 1].

Under the government's Minimum Energy Efficiency Standards (MEES), it is illegal to grant a new lease or renew a lease for most commercial properties with an EPC rating below E. In the first two months of this year, however, 200 non-domestic buildings have been registered with an EPC of F or G, rendering a significant proportion unlettable. In 2025, this figure was an astonishing 1,246, only 2% less than the previous year, demonstrating the slow pace of upgrades since 2023, when EPC E compliance became mandatory for all leases.

|

Rank - most vulnerable to energy market changes, to least |

Commercial property sector |

Volume of F & G rated asset bands lodged over 5 years, 2021 - 2025 |

Proportion of F & G asset bands against all EPCs lodged in that sector |

|

1 |

Culture, Leisure & Community |

520 |

28.5% |

|

2 |

Offices |

3,556 |

2.5% |

|

3 |

Industrial |

784 |

2.3% |

|

4 |

Education |

259 |

1.7% |

|

5 |

Other |

27 |

1.7% |

|

6 |

Storage & Warehouses |

846 |

1.6% |

|

7 |

Healthcare |

198 |

0.9% |

|

8 |

Retail |

1,339 |

0.7% |

|

9 |

Hospitality |

231 |

0.3% |

Table 1: Commercial property sectors with the highest proportion and volume of inefficient buildings.

Chart 1: The proportion of F & G asset bands lodged in 2025 for non-domestic buildings by asset sector.

On the office sector, Andrew Lloyd, Managing Director of Search Acumen, believes that the flight to quality has stalled due to pressured financial markets.

He says, “Upgrade costs are huge, often £100–£200+ per sq ft, which often doesn’t stack up financially like it once did. Lenders also tend to penalise more inefficient buildings, so you have a group of buildings fracturing off into unusable states and potentially ending up as stranded assets. Whilst some of these office buildings may be vacant, those in use, perhaps under legacy agreements, will be highly vulnerable to rising energy bills. The impact of the Middle East on oil prices and energy markets will be felt for several months, if not years, as supply chains recover long-term.”

The public sector is exposed in different ways, says Andrew.

“Our public sector is under more strain than ever before, so any unplanned cost spikes in things like energy will inevitably contribute to wider financial distress. 2023 alone saw more councils effectively go bankrupt than in the previous 30 years combined, with a further 20 councils at risk of insolvency. Meanwhile, we’ve seen our council tax bills reach record highs across the country, rising 20%[2] in the last five years, or an additional £382 per year.”

Since 2018, eight English local authorities have been issued 114 notices declaring them near-bankrupt, compared to none in the 18 years before that. In February this year, the Government agreed to issue £1.5 billion in Exceptional Financial Support to 35 councils, with Shropshire currently requiring the highest level at £121m, followed by Croydon (£119m) and Warrington (£92m)[3]. For some councils, whilst their support package for this year has come down in annual terms, across the past five-years their total EFS support remains eye-watering, including Birmingham at £898m.

Andrew continues, “Large public-facing, temperature‑sensitive services like community centres, museums and libraries make energy reductions harder without service cuts. Local authorities often manage these buildings directly, creating additional budgetary strain, as many are old, poorly insulated, and have long runtimes ingrained by purpose. Any rise in operational costs might cause retrofits to be delayed, potentially placing some of our most treasured community buildings at risk. With heavy gas use, this sector is especially sensitive to stricter non‑domestic MEES standards coming in, something Local Authorities will be considering when trying to seek relief under this year's Business Rates revaluation and to ultimately protect estates from becoming stranded assets.”

Local Authority analysis

Across England and Wales, 50% (174 out of 346) Local Authorities have registered a non-domestic EPC with an F or G asset band in the past five years. Sandwell, South Northamptonshire and South Somerset were the three worst offending locations by proportion, with 29% of all EPC’s lodged falling below the minimum standard. Blaby and Dudley closely followed at 28% [Table 3].

By volume, 12 Local Authorities jointly lodged the highest number (14) of non-domestic certificates below an E rating, including Sandwell, Wakefield, County Durham, Kirklees, Doncaster, Bristol, Buckinghamshire, Birmingham, Shropshire and Cornwall, as well as Powys and Rhondda Cynon Taf in Wales.

Energy improvements slowing

Research by the firm also uncovered the slowing rate of commercial building registrations with the highest energy performance certificates, or those typically less reliant on huge quantities of energy.

The volume of A, A+, and B registrations was growing at a rate of 26% annually up until 2024, but in 2025, this slowed to 20% [Table 2]. In fact, fewer A, A+, and B EPCs were registered in 2025 than in the two previous years, down 22% from a 2023 record high.

Andrew explains, “A, A+ and B ratings rose significantly from 2020 to 2024, peaking at 61% of all EPCs lodged in 2023. But the rate of decarbonisation of commercial assets has stalled slightly in 2025, which is disappointing to see. Whilst some of the decline could be attributed to delays in registration, it’s likely that, for many, this reflects a cooler financial climate overall, slowing down the race to retrofit.

“Headwinds from new tax policies and geopolitical uncertainty in recent times are making their mark. Without doubt, the goal of achieving an EPC rating of B or higher in all commercial buildings under MEES by 2030 feels worlds away from our current reality, heightening the risk of stranded assets and transactional complexity.”

Energy efficiency is not just about regulatory compliance, however, says Andrew. There is a significant commercial advantage once an upgrade has occurred.

“Rising energy prices don’t just hit operating costs - they accelerate obsolescence. Older, inefficient buildings are becoming unlettable faster, impacting the UK’s economic resilience when times get tough. For those with the most energy-efficient buildings, rising oil and gas prices are likely to increase the competitiveness of tenant demand, as market extremes widen.”

|

Year |

Total new lodgements rated A, A+, B |

A, A+, B as a proportion of all new non-domestic building lodgements |

Year-on-year volume change |

|

2016 |

7,646 |

11% |

4% |

|

2017 |

8,284 |

11% |

8% |

|

2018 |

11,399 |

13% |

38% |

|

2019 |

13,559 |

15% |

19% |

|

2020 |

12,202 |

17% |

-10% |

|

2021 |

15,626 |

18% |

28% |

|

2022 |

32,402 |

29% |

107% |

|

2023 |

51,188 |

37% |

58% |

|

2024 |

41,398 |

40% |

-19% |

|

2025 |

39,998 |

43% |

-3% |

Table 2: Proportion of non-domestic buildings with an energy certificate of B or higher over ten years.

To arrange a demo of Search Acumen’s commercial real estate platform, please email

Must read

Sponsored articles

Walker Morris supports Tower Hamlets Council in first known Remediation Contribution Order application issued by local authority

Jobs

")

Senior Legal Officer (Non Contentious)

Specialist Property Lawyer

Deputy Principal - Property

Lawyer - Planning

Locums

Poll

Events

05-11-2026

16-11-2026

23-11-2026

Directory